What if the stock market keeps climbing?

What if the stock market keeps climbing?

Permanent sabbaticals for everyone?

Dear Friends,

We must be in a stock bubble, right? There’s no way this could continue. That’s what I think to myself most mornings, but the stock market goes up, up, and up. It’s crazy.

For the past 20 years, I’ve been working and saving, working and saving. Finally, Iris and I agreed: let’s use 15% of our savings to take a year off. That was at the end of October, just when the stock market went gangbusters. Instead of losing 15%, our savings have gone up by more than 15%. In just 4 months!!

Surely, it will all come crashing down. Right?

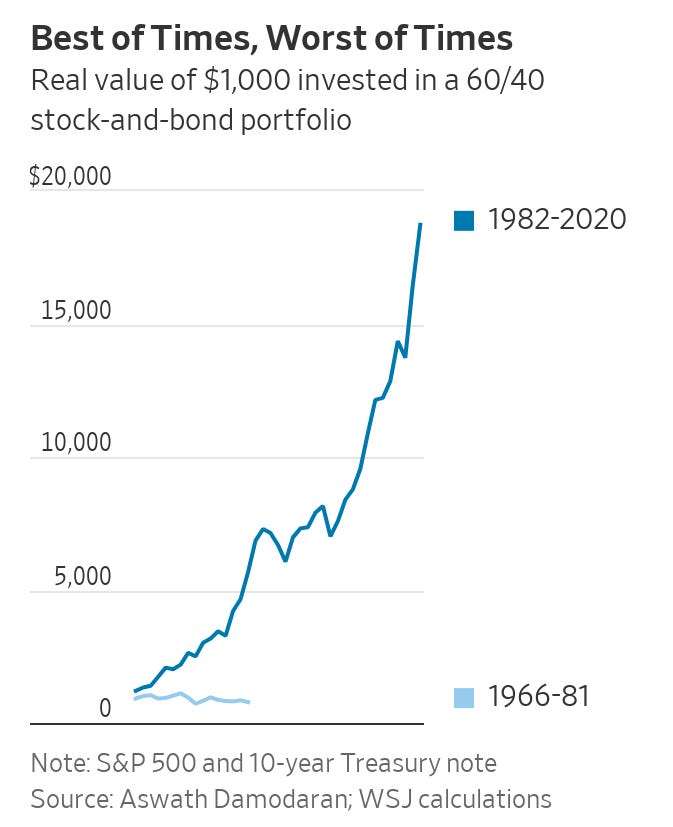

Some generations are lucky

Consider a family that invested $1,000 into a 60/40 blended portfolio of stocks and bonds in 1966 and waited 15 years for it to appreciate. By the end of those 15 years, they would have had less money in their account, just $785 adjusted for inflation. But if their kids had invested $1,000 into the same blended portfolio in 1982, 18 years later it would be worth $18,728 adjusted for inflation. Some generations are lucky.

If you started investing around 2010, you’re part of a lucky generation: Since 2010, the S&P 500 has returned 11% a year in real terms. And against all odds, it’s not stopping. If you had invested $15,000 per year in an S&P 500 index fund beginning in 2010, it would be worth $516,080.38 today — and that’s adjusted for inflation!

Or imagine that someone invested money in Japan’s stock market in 1989 and waited 35 years for it to appreciate. They would have made nothing! With inflation, they would have actually lost money. Yet, the Nikkei Index has gone up 40% in just the past year. It seems awfully unfair to the poor souls who began investing in 1989.

An optimism casino

The stock market is a measure of how optimism that companies will increase future profits.1 From The Economist:

To generate even modest real equity returns of 4% a year over the next decade, America’s firms would need to increase their underlying profits by around 6% a year, close to their best ever post-war performance.

For the past 14 years, the S&P 500 has generated real returns of 11% per year. But for the stock market to generate even just 4% annual returns over the next decade, the average company would need to see a decade of unprecedented profits and productivity while facing climate change and global politics that are far from confidence-inspiring.

An AI super-productivity boom?

The only explanation for the stock market’s performance is faith in transformative AI and robotics. Holden Karnofsky says we’re wrong to think about economic growth like this:

But if we look at the previous 5,000 years, we see that economic growth was actually stable until the Industrial Revolution kicked it into overdrive. How do we know when we’re on the brink of something as transformative as an Industrial Revolution?

I sure don’t know! But I’m intrigued by Geoffrey Hinton’s claim that:

“The Industrial Revolution was when we could reproduce physical labor with machine labor. And now we can reproduce intellectual labor with machine labor. And it’s a revolution of at least the same scale.”

Karnofsky explores the economic implications if you could produce an infinite number of “digital people” who are as accurate and more productive than biological people.

We don’t know that this is possible. Maybe computers and brains are fundamentally different. Or we’re not able to manufacture enough chips. Or there isn’t enough energy to power all those digital people. But none of these limitations seem likely. Dwarkesh Patel’s latest conversation with DeepMind’s Demis Hassabis lays out a sober, straightforward path to get to scalable human-level artificial intelligence by 2030.

If that’s true, then a 6% annual increase in profits over the next decade for most companies seems rather small. In that case, the stock market is undervalued. Then what?

Perhaps we could shift our focus from economic growth to economic redistribution, psychological well-being, and social inclusion. Or we might end up destroying the planet and focusing on space colonization. Either way, it promises a wild future.

Sabbaticals and Buffet baby bonds for all

But seriously, what if ours was the last generation that had to work for financial security? I know, I know, it sounds absurd. But I can’t think of a single job, other than governance and courts, that couldn’t be replaced by software and robots.2

In that case, perhaps over time. we’ll all be doing what I’m doing now: not working, reading books in the hammock, hanging out with friends, sharing thoughts online, going for long walks.

Warren Buffet does not believe that AI will super-charge the economy — or at least not the companies he invests in. He warned shareholders last month that there is “no possibility of eye-popping performance in the years ahead.”

Warren Buffet is 93 years old and continues to eat burgers and drink Diet Coke most days. He’s worth $132 billion and says he still plans to give it all away when he dies. Where will it go? It seems increasingly unlikely that most of it will go to the Gates Foundation, as originally planned.

One idea, covered by the Wall Street Journal is to create a world savings bank for children. You could call it “Buffet’s baby bonds” — putting over $1,000 into an investment account for more than 100 million children born into poverty, and then let it grow until they reach a certain age.

Who knows, in the grand scheme of the world economy, even Buffet’s $132 billion isn’t much. But for a kid in Sudan or even rural Bolivia, tapping into an investment account worth $6,500 when you’re 18 could be life-changing.

We will see how this week’s newsletter ages when I open up the time capsule in 20 years. Maybe the stock market crashes, and I go back to making lattes to save up enough for retirement. Maybe Russia launches a nuclear weapon from a satellite. Or maybe I never have to work again for financial reasons, and maybe that slowly, eventually becomes true for everyone.

Whatever the future, I hope you treat this coming weekend like a full sabbatical.

David

They could either sell to more people, or become more productive by making more with less. Since fertility rates are falling faster than expected, investors are betting on increased productivity.

I suppose governance and judges could also be replaced by software that’s less prone to bias and megalomania, but I hope we stick with the flawed humans when it comes to making moral decisions.